Proposition 19

Understanding how Proposition 19 affects property tax implications tied to your property transfer is an important consideration when buying or selling a home.

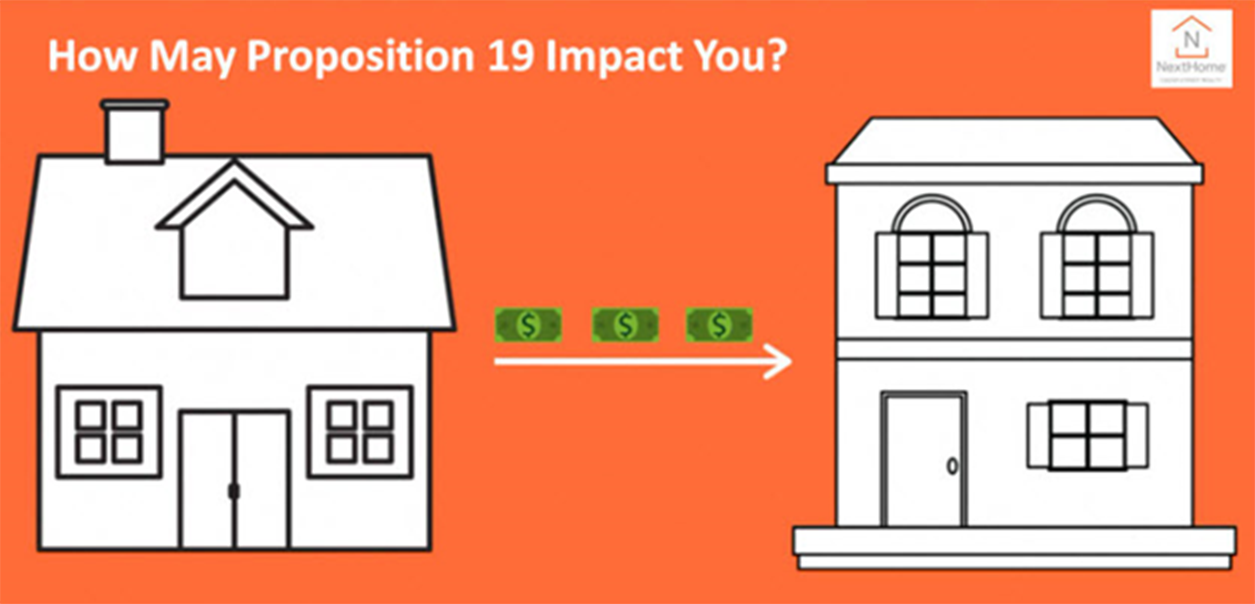

Starting April 1, 2021, homeowners who are 55 or older or those who lost their home in a natural disaster are allowed to transfer the taxable value of their primary residence to a new home in California. If you purchase a more expensive home, the tax bill will go up but by a lower amount than for other buyers. This kind of tax transfer can be done three times and homeowners have two years to sell their current home and buy a new one.

The prior rule limited this exemption to a one-time transfer within the same county or between certain counties and only if the replacement property was of equal or lesser value.

Can my client buy/sell now and take advantage of the tax portability benefits before April 1, 2021? If you wish to obtain the tax benefits of Prop 19 for a transaction that closes before April 1, 2021, whether it is buying or selling a property, I would recommend speaking to a qualified California real estate attorney.

If the replacement property is of equal or lesser value, does the tax basis of the replacement property change? No. The taxable value of the original property may be transferred and become the taxable value of the new one.

If the replacement property is of greater value, how is the new taxable value calculated? The new taxable value is calculated by adding the difference between the full cash value of the replacement property and the original property to the original taxable value. For example, if a seller of an original property has a $300,000 taxable value and a full cash value of $1M and then buys a replacement property for $1.5 M, the taxable value of the replacement property would be $800,000.

Can a replacement property be purchased prior to the original primary residence being sold? Yes. This is how the current rule under Prop 60 works and Prop 19 uses nearly identical language.

How does Prop 19 affect the rules on intergenerational transfers to children or grandchildren? Prop 19 eliminates the ability for a home to pass from a parent to a child or a grandchild without reassessing the home value unless it’s the child’s or grandchild’s primary residence. If the child or grandchild doesn’t live in the inherited home and instead chooses to rent it out, the tax value can be re-assessed. Right now, family members can transfer a home and the property value won’t be reassessed. They can also transfer other rental or commercial properties and exempt up to $1 million of the assessed value.

If the property is more than $1M over the original tax basis, what is the new taxable basis? The new taxable basis will be the assessed value of the property at the time of transfer minus $1M.

When do these new rules on intergenerational transfers apply? The new changes to property transfers among family are set to begin on February 16, 2021.

Where may a claim to transfer a tax basis be made? Claims may be made with forms provided by the local county assessor’s office.

Source: California Association of REALTORS®